A new proposal is gaining attention: extending home loan terms to 50 years rather than the more typical 30. The idea is that a longer term could reduce monthly mortgage payments, potentially helping more people afford a home.

According to MarketWatch, for a median-priced U.S. home costing around $415,200 (with 20% down and a 6.2% interest rate), the monthly payment on a 30-year mortgage would be approximately $2,813. A 50-year mortgage would lower that to about $2,577.

Supporters argue this could ease the path to homeownership. Critics suggest it could delay equity building and ultimately cost buyers more in interest. As USA Today notes, the idea is controversial, especially among financial experts.

How do the numbers compare?

Below is a comparison using a loan amount of $332,160 (80% of the $415,200 median home price), assuming a 6.2% fixed rate:

| Mortgage Term | Monthly Payment | Time to $50K Equity |

|---|---|---|

| 30 Years | ~$2,813 | ~8 years |

| 50 Years | ~$2,577 | 20+ years |

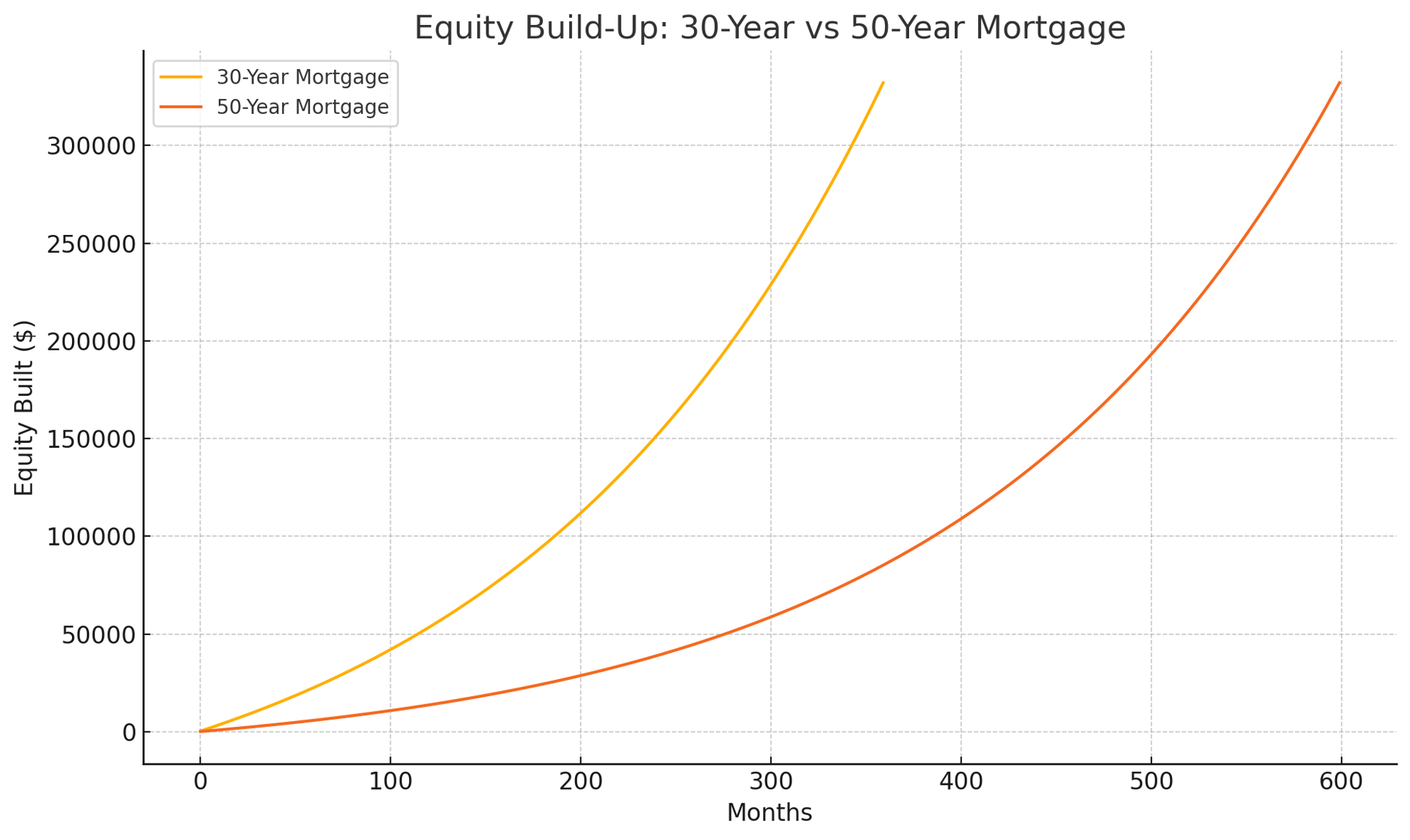

While the 50-year mortgage trims about $236 off monthly costs, it takes more than twice as long to pay off the first $50,000 in principal, based on data modeled by MarketWatch.

Visual: Equity build-up comparison

The following graph illustrates how quickly a homeowner builds equity with a 30-year mortgage compared to a 50-year mortgage:

Potential advantages

-

Lower monthly payments can provide flexibility and affordability, especially for first-time buyers or those in high-cost markets.

-

Extended loan terms might help people qualify for larger homes, assuming lenders approve.

Trade-offs and risks

-

Slower equity build-up: As MarketWatch notes, this significantly delays ownership in the home.

-

Greater interest costs: Stretching a loan over 50 years means paying interest for 20 more years.

-

Regulatory uncertainty: HousingWire reports that such loans could conflict with current federal lending guidelines.

-

Resale timing: The average U.S. homeowner sells after about 12 years. Newsweek notes that those who sell before breaking into substantial equity may see little benefit.

Who it might help

-

Buyers needing lower monthly payments in the short term

-

Households planning to stay put for decades

Who it might not help

-

Buyers planning to move within 10–15 years

-

Homeowners prioritizing rapid equity build-up or long-term savings

Final thoughts

A 50-year mortgage offers lower monthly payments, but that comes with long-term costs. It’s important to weigh this trade-off carefully. As USA Today points out, many experts urge caution, particularly for those who may not stay in their home long-term or who hope to build equity quickly.

Have questions about what this could mean for your home search or finances? Contact Camille Canales at [email protected] or call 773.232.5282 for personalized insights.